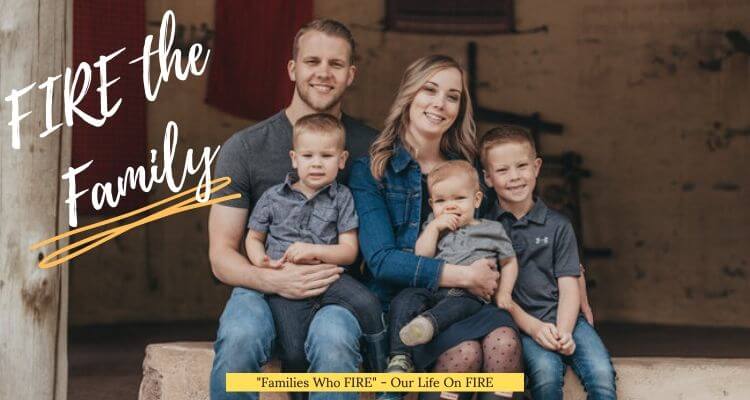

Families Who FIRE: Nick From “FIRE The Family”

In this Families Who Fire Interview we talk to Nick from FIRE The Family.

This young family from Texas includes Nick, his wife Kayla, and their three boys. Nick and Kayla have been married for 10 years and have worked together during this time to organize their finances and come up with a plan to FIRE.

Nick is a veteran and between himself and Kayla they have earned 5 degrees with miraculously no student loan debt.

Together they have worked hard over the years to increase their financial education, advance their careers, and significantly boost their earnings. As a result, they are able to save about 40% of their income to help them along their path to FIRE.

On their blog, FIRE the Family, Nick and Kayla are there to walk you through your journey to Financial Independence. They offer an extensive amount of information to get you started and keep you motivated.

I am really excited for you to get to know this family. Being a family of 5 with 3 young children can be challenging. But they show you that with hard work and determination you can reach your goals.

Now, let’s get this interview started:

Some of the links below are affiliate links. As an Amazon Associate we will earn a commission from qualifying purchases if you decide to make a purchase through our link, at no additional cost to you.

What are your occupations and income level?

I’m an Account Manager in the software as a service industry and make about $90,000 per year. My wife is a kindergarten teacher and she earns about $50,000 per year.

When did you start your FIRE journey and what motivated you to start?

We’ve worked on being intentional with our money for the past 10-years. We struggled in the early years. Then had almost no money while going back to college after separating from the military.

I discovered FIRE shortly after starting my first job out of college as a Business Development Rep making 50-100 cold calls per day. After a few promotions and drastically increasing my income, I really wanted to keep our expenses the same and save the surplus.

After plugging numbers into a FIRE calculator I was hooked.

My wife was ready to start teaching after being a hybrid stay at home mom and part time worker for 10-years. When she started teaching our household income grew by about 50%.

We determined we could pour money into savings/investments and build real wealth much quicker than if we allowed our expenses to increase with our incomes.

The end game for us is to be able to make decisions independent of the income these decisions will provide to us.

Work will always be in the picture. But we want the nature of our work to be up to us, not up to the restrictions that consumer debt would place on us.

Did having children change your financial game plan?

Yes, most definitely. We had our first kid at the age of 21. Then at 25 and at 27. I wouldn’t say it changed the plans we had, because we didn’t really have a plan at that point. But it forced us to get a plan really fast.

Once we started having kids, I knew I had to get our finances in gear. And since then I’ve pushed myself to grow my income, and work towards a financial future for their benefit.

What strategies do you use to reach your goal of Financial Independence?

For us, it begins with financial communication. My wife and I have really excelled in that aspect of our marriage. Our financial goals are well aligned and we’ve remained laser focused on them.

Next, is our budget. We need to be able to see how much cash we’re bringing in each month and how much is leaving the household in the form of expenses.

By running a zero-based or every dollar budget, we are able to ensure we’re spending below our means while allocating the delta between income and expenses to investments and savings.

FInally, by working to increase our income via education, promotion and hard work we’ve been able to drastically increase that delta between income and expenses.

We found that expenses can only be reduced so far, but income can increase infinitely. I don’t believe enough people focus on the income part of the equation because it’s more difficult.

How have you and your wife been able to significantly increase your income in order to build up your financial nest egg?

Just 3-years ago we were earning very little as a household. This was because I was finishing up my bachelors degree and was living off of my Post 9-11 GI Bill. I worked as well, but it was paid in a non-taxable living stipend.

It’s during this time that I described us as “being in a slingshot.” It felt as if we were being pulled back temporarily and it would allow us to move forward rapidly.

I felt that given the right opportunity, I would be able to rapidly grow my income and that meant finding a job in software sales or medical sales. After interviewing for both, I accepted an offer to make cold calls for a software company. I quickly promoted a few times through our growing company and my income followed.

We decided that my wife would start teaching full-time and that grew our income by quite a bit as well.

The income grew as a result of two eager adults joining the workforce. Base salary plus commission doesn’t hurt as I’m able to control a large portion of my financial destiny.

I earned an MBA degree last year and my wife will have her Master’s in Education in just a few months. So we should be able to fuel further income growth over the coming years, but never at the risk of family time.

Luckily, she enjoys a lot of time off as a teacher and I work from home. We’re able to find a very nice balance of income growth and time with our boys.

Are there any particular blogs, podcasts, books, etc that you have found helpful and inspirational to reach FIRE?

If I had to name one creator that I listened to a lot, it would have to be Listen Money Matters. Mostly because they talk a lot about building websites and additional income streams and that’s my big interest at the moment.

I really enjoy reading classic personal finance literature. The Intelligent Investor is what really got me interested in investing in my early 20’s (although I could barely understand a word of it).

Reading classic literature like the Bible and stoicism have been really helpful in balancing the desire to build wealth with contentment and mindfulness and being a good steward of our money. These are of course where modern personal finance concepts originated, might as well go to the source.

To be honest, I do a lot of my research independent of the more mainstream FIRE bloggers. The FIRE basics can be well understood without the commentary in my opinion and a lot of it is reiterated from a primary fountainhead like Dave Ramsey.

“Budget, save for emergencies, spend less, earn more and invest like crazy is really all anyone needs to know. The hard part is executing it consistently over time.”

Nick from Fire the Family

So I use websites like Investopedia, published studies and the personal finance subreddit to better understand personal finance from a textbook, data-driven conceptual level as well as the struggles people are currently having with the implementation side of it.

When do you expect to reach FIRE?

There’s going to be many mile markers along the way. Right now, we have a fully funded emergency fund, we’re investing 30-40% of our income and when daycare is over, will be closer to 50%. I think we will be able to say we’ve achieved financial independence in 10-15 years. Statistically, it’s usually sooner than you expect, but a lot is dependent on market returns and income growth.

Do you plan on retiring when you reach FI? If so, how do you plan on spending your time?

It depends on what you mean by retire. If retirement means I spend my working time on firethefamily.com rather than working for someone else, then yes, I would retire. If it means spending 40-years relaxing and not producing anything of value for society? Then no, I wouldn’t retire.

To me, retirement means being able to choose who I work for (including myself), where we live, and how we spend our time, independent of the restrictions a lack of money can put on us.

What has been the most challenging part of your journey?

Patience. Being patient to watch our investments grow over time has been the hardest part for me. Not jumping on the newest get rich quick fads or trying to pick the next Tesla or Netflix. It’s getting easier as I get older, but I struggled with that in my early 20’s.

What advice would you give to other families who are trying to reach FIRE

Learn the basics and get started today. Financial communication is the most important part in my opinion. If you never figure that out, you could end up in a tough spot down the road and a divorce will split your assets in half. That won’t get you any closer to achieving financial independence.

My main recommendation is Budget, Emergency Fund, Savings Rate, Total Stock Market. If you do just that with minimum effort, you can achieve financial independence some day in the future. The fun part is when you start to tinker with it and make it more efficient. You can achieve your goals much faster.

I want to thank Nick for giving some great insight into how to work together as a family to reach the ultimate financial milestone of FIRE.

If you would like to connect with Nick and Kayla you can find them on Instagram. You can also continue to follow them on their FIRE journey by checking out their blog, FIRE The Family.

Related Financial Articles:

1. How to build a financial legacy even if you’re not rich

2. How to successfully create a budget today

3. Families Who FIRE: The CampFIRE Family

3 thoughts on “Families Who FIRE: Nick From “FIRE The Family””

great interview!

really a wonderful and a quality interview. thanks for putting this together!

Thank You! I’m happy to hear that you enjoyed the interview.